Request For Payment Return Codes

How to Request For Payment Return Codes

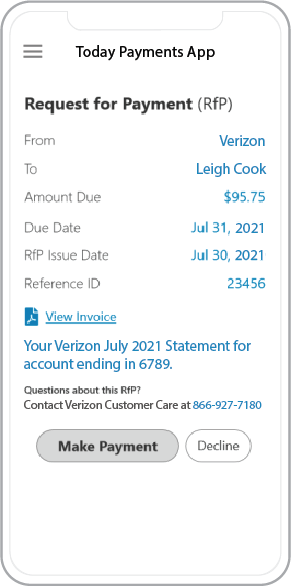

Request for Payment, a new standard for digital invoicing facilitating real-time payments RTP ® and FedNow ®

payments that are instant, final (irrevocable - "good funds") and

secure.

Request for Payment, a new standard for digital invoicing facilitating real-time payments RTP ® and FedNow ®

payments that are instant, final (irrevocable - "good funds") and

secure.

When you encounter Request for

Payment (RFP) reject codes during the "Receiving" phase of

funding transmissions with banks, payee, and payer, it's

crucial to take specific actions to address the issues

before attempting to clean and sync the message data. Here

are general steps you might consider:

1. Identify Reject Codes:

- Review the reject codes

provided by the bank to understand the specific reasons

for the rejection. Each code indicates a particular

issue that needs to be addressed.

2. Isolate and Document

Issues:

- Document each reject code

along with a brief description of the issue it

represents. This documentation will be useful for

tracking and resolving the problems.

3. Review Payer and Payee

Information:

- For reject codes related to

payer or payee information, carefully review the

details provided in the RFP. Verify that payer and

payee information is accurate, complete, and matches

the records on both ends.

4. Correct Invalid

Information:

- If the reject code

indicates invalid or incomplete information, take

corrective actions to ensure that all required data

fields are accurate and properly filled out. This may

involve updating payer or payee details.

5. Communicate with Payer and

Payee:

- In cases of invalid payer

or payee information, reach out to both parties to

resolve any discrepancies. This may include updating

contact details, addresses, or account information.

6. Address Insufficient

Funds:

- If the reject code is

related to insufficient funds, communicate with the

payer to address the issue. This may involve requesting

additional funds, alternative payment methods, or

negotiating payment terms.

7. Check for Duplicate

Transactions:

- If the reject code

indicates a duplicate transaction, review recent

submissions to ensure that the same request has not

been submitted multiple times. Avoid resubmitting

duplicate transactions.

8. Verify Payment Amount:

- For reject codes related to

payment amount, verify that the specified amount is

within acceptable limits and meets the transaction

requirements.

9. Adhere to Request Format:

- Ensure that the request for

payment adheres to the required format and standards

specified by the bank. Correct any issues related to

the format of the message.

10. Update Payment Reference:

- If the reject is due to an

error with the payment reference or invoice number, update

the information to ensure accuracy.

11. Confirm Payee Account

Status:

- If the reject code indicates

that the payee's account is closed, confirm the status of

the payee's account. If necessary, obtain updated account

information.

12. Correct Bank Account

Information:

- For reject codes related to

bank account information mismatches, verify and correct the

bank account details to ensure accuracy.

13. Document and Record

Actions:

- Keep detailed records of the

actions taken to address each reject code. This

documentation is crucial for tracking resolutions and

ensuring compliance.

14. Clean Data and Reattempt:

- Once the identified issues are

resolved, and the data is cleaned, you can reattempt the

transmission of the Request For Payment.

15. Continuous Monitoring:

- Implement continuous

monitoring and validation processes to prevent similar

issues in future transactions. Regularly update and review

data to ensure accuracy.

Remember, these steps are

general guidelines, and specific actions may vary based on

the nature of the reject codes and the processes

established by your bank or financial institution.

Effective communication and a proactive approach to

resolving issues are essential for successful Request For

Payment transactions.

ACH and both FedNow Instant and Real-Time Payments Request for Payment

ISO 20022 XML Message Versions.

The versions that

NACHA and

The Clearing House Real-Time Payments system for the Response to the Request are pain.013 and pain.014

respectively. Predictability, that the U.S. Federal Reserve, via the

FedNow ® Instant Payments, will also use Request for Payment. The ACH, RTP® and FedNow ® versions are "Credit

Push Payments" instead of "Debit Pull.".

Activation Dynamic RfP Aging and Bank Reconciliation worksheets - only $49 annually

1. Worksheet Automatically Aging for Requests for Payments and Explanations

- Worksheet to determine "Reasons and Rejects Coding" readying for re-sent Payers.

- Use our solution yourself. Stop paying accountant's over $50 an hour. So EASY to USE.

- No "Color Cells to Match Transactions" (You're currently doing this. You won't coloring with our solution).

- One-Sheet for Aging Request for Payments

(Merge, Match and Clear over 100,000 transactions in less than 5 minutes!)

- Batch deposits displaying Bank Statements are not used anymore. Real-time Payments are displayed "by transaction".

- Make sure your Bank displaying "Daily FedNow and Real-time Payments" reporting for "Funds Sent and Received". (These banks have Great Reporting.)

Each day, thousands of businesses around the country are turning their transactions into profit with real-time payment solutions like ours.